My husband and I are having our first baby. Apart from the sheer terror on my behalf of hoping to keep a human being alive, there are also many other considerations that we never had to think about before. Not to mention the many baby ‘essentials’ that I have never heard of and now spend hours of searching what they are for and what is the most appropriate one for my little one.

This also led me to think about the many women that go through this and what are some financial implications that we now have to think about.

Pre-pregnancy planning

Kids are expensive. According to a 2023 report[1], you should have saved around $31,000 before the child’s arrival. Yikes, that’s a lot. On top of this, parents will spend an average of $12,823 per year on their kids.

Budgeting

With the increase in outgoings, some families may also have a decrease in income if there’s parental leave involved. With that in mind, it may be a good idea to have your budget organised before the baby arrives. How much do you need to allocate for your current expenses and how much to allocate once the baby is here? Are you still going to be comfortable with the reduction in income? Think about your cash flow management – is it necessary to reduce some debt?

Tip – if you have a house and would like the option to reduce your outgoings, have a chat to your lender about a mortgage holiday/deferred payment.

House hunting

With the pending arrival, it can bring about the conversation of where you would like to raise your kids. For some of us, it might mean moving to a bigger place. For some others, it means buying a home to raise a family in. This may involve saving for a down payment and having a buffer to cover the ongoing costs. Some lenders may only consider one income during this time, so do look around for what gives you the best option.

Selling assets

If you are having to sell some assets (such as investment property or shares) to reduce some debt or buy a home, do be mindful of how this will impact your tax bracket and eligibility for government benefits such as childcare subsidies and paid parental leave.

Insurance

The ol’ private vs public debate. Here’s a good podcast if you want to have a listen about the benefits of private care: https://australianbirthstories.com/podcast/episode-399/

Do be mindful that there is typically a waiting period of 12 months with most policies and that timeline is inflexible.

Pregnancy budgeting

Private vs public

If you decide to go down the private route, don’t forget to dig a little deeper into your entitlements as they do vary between insurers. Private insurance for pregnancy typically covers the cost of the actual private hospital stay and procedures. Would your policy also cover the anaesthetist fees if you require their services? What if your baby requires care at the hospital, does your policy cover that? Check with your insurer for the finer details, and while you’re at it, would your baby be automatically added to your policy or is this something you have to do after birth?

Obstetrician fee is usually a separate payment and paid before birth. Different doctors charge different amounts and you may be able to pay for the fees in instalments. Medicare do provide rebate for a (small) portion of the fees.

The public system is free through Medicare. It covers costs for the obstetrician, midwives and hospital stay. What an amazing country we live in!

For me, I am currently going through the public system. But after experiencing some complications with my baby and getting a little lost between switches with two hospitals, I am still considering going the self-funded private route, which was about $10,000 for me which includes the obstetrician and hospital stay (and not much else) There has to be something said for the continuity of care that you would get through the private system. But I have to say the clinical care I have received so far at Westmead Public Hospital has been amazing.

Oh, I must not forget to mention hospital parking fees…

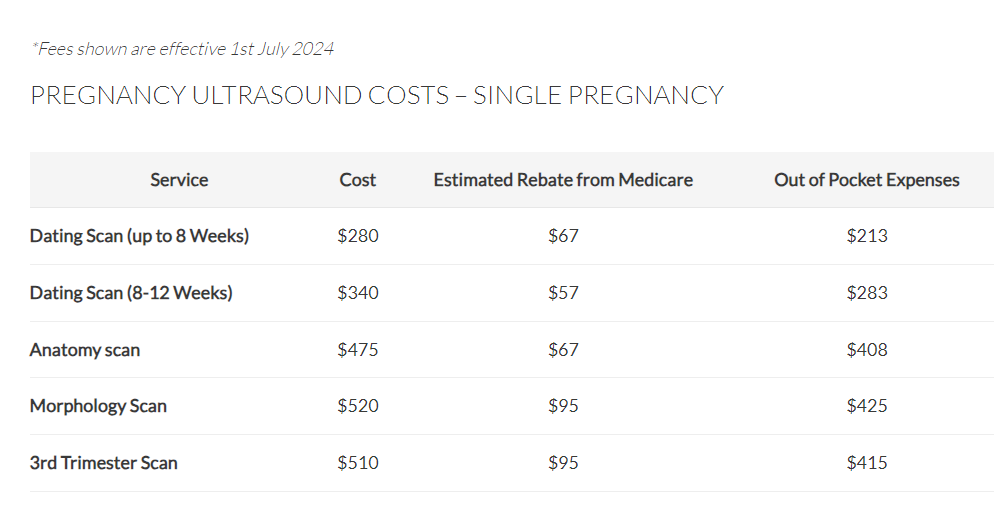

Scans and tests

There is something a little magical looking at the scan images of your baby, but the same thing can’t be said for the many blood tests you have to do. Medicare do cover portion of the fees, but not all scans or tests are covered. Here’s an example of the type of fees you may have to pay. (twins will be a bit more expensive…)

Maternity clothing

The day that my jeans refused to button up no matter how much I tried to force it was the day I realised I do need new clothes to last me through the rest of the pregnancy. Everyone is different when it comes to clothing choices – they are a huge part of our identify after all. However, another thing to add to your budget.

Baby essentials

We are lucky to have some friends that had babies not too long ago. Everyone had their essentials list. Some things are non-negotiable – like cots, clothing, prams and nappies. But everyone did have their own preferences for certain things that they couldn’t live without so you will have to make a judgement call on what you need. For a great resource, check out https://raisingchildren.net.au, which is supported by the Australian government.

Financial values

This is not quite a budgeting item but was an essential item for me. My husband and I sat down to discuss what values are important for us, and what values we would like our child to have. What financial values would you like your child to have? And how would you teach them those values? Are you going to set up a savings account or an investment account for your child?

Government support and entitlement

There are various government benefits and entitlements available to new parents in Australia, such as Paid Parental Leave, Child Care Subsidy, and Family Tax Benefit. These can be great to ease some of the financial stress during early stages of parenthood.

https://www.servicesaustralia.gov.au/parental-leave-pay

https://www.servicesaustralia.gov.au/child-care-subsidy

https://www.servicesaustralia.gov.au/family-tax-benefit

There are eligibility criteria to meet so do check the websites for the latest information.

Maternity leave and return to work

In most instances, Australian workers are eligible for 12 months unpaid parental leave (make sure you read your contract if you’re an employee) and you should take this within 24 months of the birth of the child. I don’t think my Scandinavian husband find this very generous, but that’s discussion for another day!

When you are sleep deprived with your bundle of joy, returning to work may be the last thing on your mind. However, studies have shown that women often face a 5-10% income reduction per child, in the first decade of parenthood. So it’s not only the maternity leave impact to consider, but also the ongoing childcare responsibilities.

Some considerations for you to think about:

- Are there ways you can supplement your income?

- If you are planning to take maternity leave, and you have a partner, can they contribute towards your superannuation?

- If you are planning to take extended period off, how does this affect your long-term earning potential?

Parenthood is one of the biggest milestones in someone’s life. Same as you, I am bracing myself for the big transition and the new adventures ahead. Let’s make sure we can plan ahead, budget well and consider the financial aspects as carefully as we can so we don’t get too many unexpected surprises. If you need a budgeting tool, make sure you check out the Resource centre for the budget planner.

[1] https://www.choosi.com.au/life-insurance/articles/budgeting-for-baby